Truebill markets itself as a tool to help users save money, but its billing practices have drawn legal scrutiny and left many subscribers paying for a service that underdelivered on its promises. Understanding what a class action lawsuit is becomes relevant here, as consumers who were charged unfairly may have grounds to recover those costs.

There is a more direct way to reclaim money owed by companies. Rather than paying a monthly fee to manage subscriptions, consumers can take action through Sparrow and join class action lawsuits to claim settlements they are already entitled to.

Table of Contents

- What Is Truebill, and What Does It Offer?

- Why Do People Look for Truebill Alternatives?

- What Should You Look for in Truebill Alternatives?

- 10 Truebill Alternatives for Better Money Management

- Tips for Choosing the Best Truebill Alternative

- How Sparrow Makes Recovering Unclaimed Money Simple

- Start Finding Money You May Be Owed with Sparrow

Summary

- Subscription tracking apps like Truebill (now Rocket Money) offer genuine utility in identifying forgotten recurring charges, but their cost structures often work against users. Premium plans run $3 to $12 per month, and successful bill negotiations carry an additional 35 to 60 percent fee on first-year savings. A user who saves $300 on a cable bill can end up paying back to the platform close to $180, which considerably narrows the actual financial benefit.

- Detection and cancellation are two separate problems, and most budgeting apps solve only the first. Free users must handle cancellations manually, while premium users rely on a concierge service that reviews on Trustpilot (averaging around 3.3 stars across thousands of entries) describe as inconsistent, with active subscriptions mislabeled as canceled and charges continuing after confirmation. Surfacing a subscription and actually stopping it are not the same outcome.

- Data accuracy creates a real financial risk when it fails. More than 60 percent of Americans now use a budgeting app or tool to manage their finances, according to Academy Bank’s 2025 banking trends research, which means the stakes for real-time transaction accuracy are high. When syncing delays cause a dashboard to reflect outdated balances, users making spending decisions based on that data are working from information that does not match their actual accounts.

- Privacy tradeoffs in subscription management apps are frequently underexplained during onboarding. Linking full bank and credit card accounts through third-party aggregators like Plaid gives platforms visibility into every transaction, not just recurring ones. Most users accept default permissions because the setup flow presents broad access as a requirement, but read-only modes and granular permission settings are available on some platforms and represent a meaningfully lower exposure profile.

- Unclaimed class action settlement money represents a category of consumer recovery that budgeting dashboards do not address at all. According to Sparrow via GlobeNewswire, 1 in 10 Americans has unclaimed money waiting to be recovered, spread across state databases, dormant accounts, and settlements tied to services people use regularly. The barrier is rarely awareness of the concept, but rather the friction of identifying eligible cases and completing the filing process before deadlines close.

- The gap between knowing a settlement exists and actually filing a claim is where most eligible consumers lose out. Settlements like the Disney and YouTube TV antitrust case (up to $200) or Toyota Airbags (up to $250) require completed forms to be submitted before specific deadlines, and the administrative design of most claim portals was built for processing volume rather than for consumer ease. Join class action lawsuits addresses this by scanning for eligible settlements, pre-filling claim forms, and handling physical mailing, so the filing step that most people abandon actually gets completed.

What Is Truebill, and What Does It Offer?

Truebill (now rebranded as Rocket Money) seamlessly connects to your bank and credit card accounts to show every recurring charge, giving you powerful tools to cut unnecessary subscriptions, negotiate lower rates, and save what’s left over. It’s essentially a financial dashboard built for people whose money moves faster than their attention.

💡 What It Does: Truebill/Rocket Money acts as your all-in-one financial command center — surfacing hidden charges, flagging wasteful subscriptions, and putting real savings back in your pocket.

“Truebill connects to your accounts to reveal every recurring charge — giving you the tools to negotiate, cancel, and save on autopilot.” — Core Product Promise

🔑 Takeaway: Whether you know it as Truebill or Rocket Money, this tool is critical for anyone who wants full visibility over where their money is going — especially with recurring charges that quietly drain accounts every month.

How does Truebill catch hidden subscription costs?

The subscription tracking feature catches forgotten free trials that turn into paid plans: easy $15 losses that accumulate across services. Truebill’s automatic detection scans linked accounts and flags recurring transactions so nothing escapes your statement. Premium users can have a concierge team handle cancellations by contacting providers directly, typically within a few days.

What spending tools does Truebill offer beyond subscriptions?

Spending insights and budgeting tools give you a clear view of your financial life. Transactions from all connected accounts appear on a single dashboard, sorted by category, flagged for unusual activity, and organized around an upcoming bills timeline. Truebill has processed 73,464 transactions, demonstrating active platform use. Custom budgets, auto-categorization rules, and split transaction tools enable Premium users to manage groceries, utilities, and freelance expenses with precision.

What bill negotiation feature does Truebill offer that most users miss?

Bill negotiation surprises users most because it carries no upfront risk. Submit an internet, cable, or phone bill, and Sparrow’s team negotiates a lower rate on your behalf. You pay only if they succeed, typically 35 to 60 percent of the first year’s verified savings. This performance-based model removes hesitation to try a new financial service, and users report meaningful monthly reductions that add up over the year.

How does Truebill build a complete financial picture beyond budgeting?

Automated savings and credit monitoring round out the platform’s value. Smart Savings analyzes your cash flow and moves small amounts into an FDIC-insured account at optimal times to build emergency funds without triggering overdrafts. Credit score tracking, full report history, and net worth monitoring across linked accounts provide a complete financial picture beyond checking a balance. Y Combinator’s company profile for Truebill notes the company was founded in 2015, reflecting nearly a decade of refinement.

What category of money owed to consumers do most financial platforms overlook?

Most people try to recover money by spending less or negotiating their bills. But a whole group of money owed to consumers never appears on budgeting dashboards: class-action settlements. Companies settle legal disputes every year, and payouts often go unclaimed because people don’t know the case exists or find filing too difficult. Platforms like Sparrow remove that friction by helping you discover settlements you qualify for and file claims quickly, converting legally entitled payouts into money you receive.

Related Reading

- What Is A Class Action Lawsuit

- What Is A Class Action Settlement

- How Do Class Action Settlements Work

- How To Find Unclaimed Money

- Are Class Action Settlements Taxable

- Doge Transparency FOIA Lawsuit

- General Motors V8 Engine Lawsuit

- Shannon Sharpe Lawsuit

- Google Android Cellular Data Lawsuit

- Pima County Sheriff Lawsuit

- Ozempic Lawsuit

Why Do People Look for Truebill Alternatives?

The most common frustration centers on cost. Business Insider reports that Rocket Money charges $3 to $12 per month for its premium plan, plus a 35 to 60 percent cut from successful bill negotiations. For a user who saves $300 on an annual cable bill, the negotiation fee alone costs $180.

“Rocket Money takes a 35 to 60 percent cut from successful bill negotiations — meaning a $300 savings on a cable bill can cost the user $180 in fees alone.” — Business Insider

🔑 Takeaway: Paying $180 to save $300 means you keep only $120 of your own money. For many users, that math doesn’t add up.

⚠️ Warning: The $3–$12/month premium fee is charged on top of the negotiation cut, meaning your total annual cost could far exceed what you’d expect from a “budgeting” app.

💡 Tip: Before committing to Rocket Money’s premium plan, calculate your savings potential against the 35–60% negotiation fee to determine if an alternative tool offers better value for your situation.

Does Truebill actually cancel subscriptions reliably?

The failure point is the gap between finding a problem and fixing it. Rocket Money reliably finds subscriptions, but canceling them is another matter. Free users handle cancellations manually, defeating the purpose. Premium users get concierge service, yet Trustpilot reviews (averaging 3.3 stars) describe active subscriptions mislabeled as canceled, charges continuing after confirmation, and slow support responses.

Account syncing compounds the problem. When transaction data arrives days late or is miscategorized, the spending dashboard no longer reflects reality. According to Academy Bank’s 2025 banking trends research, more than 60 percent of Americans use a budgeting app to manage their finances, making accuracy a high stakes game. A tool requiring constant manual correction wastes time rather than saving it.

What privacy and fee risks come with using Truebill?

Privacy concerns add another layer. Connecting multiple financial accounts through third-party aggregators like Plaid means sensitive data passes through systems outside the user’s control. For people frustrated by unexpected charges, granting full account access to an app with BBB complaints about disputed fees feels like a poor trade-off.

What are people really looking for beyond Truebill?

The pattern across all complaints is the same: money that should stay with the consumer goes elsewhere. Most people don’t realize they qualify for class action settlements tied to companies they’ve used or products that overcharged them. Sparrow addresses that gap directly, scanning for settlements you qualify for and handling the filing process so the money you’re legally owed reaches you.

What people seek when looking beyond Rocket Money is not a cheaper app, but a more complete system for recovering what is theirs.

What Should You Look for in Truebill Alternatives?

Choose a Truebill alternative based on five critical criteria: accurate detection, honest pricing, real privacy controls, verifiable cancellation results, and clean exit options. Miss even one, and you may end up paying more than the subscriptions you were trying to cut.

“The best subscription manager should cost you less than it saves — in money, time, and peace of mind.” — Core Evaluation Principle

🎯 Key Point: Every Truebill alternative must be evaluated on all five criteria — a tool that excels at detection but fails on privacy controls is not a safe choice.

⚠️ Warning: Many subscription managers advertise “free” plans but charge a percentage of savings — meaning the more money they find, the more you owe them. Always verify the true cost structure before connecting your accounts.

Where does Truebill’s detection actually fall short?

The failure point is the gap between what an app claims to find and what it surfaces. Most subscription trackers catch obvious charges like Netflix and Spotify. The harder problem is the $7.99 wellness app billed three times under a parent company name, or the annual fee that renewed quietly eleven months ago. Reliable detection requires consistent re-scanning across linked accounts, clear merchant categorization, and alerts that fire before renewals hit rather than after. Without that, the tool offers a useful-looking dashboard while missing the charges doing the most damage.

Does Truebill’s pricing structure actually work in your favor?

Pricing structure deserves equal scrutiny. A flat monthly fee of $4 or $6 is straightforward. A success fee of 35 to 60 percent of your first year’s savings, collected upfront, differs fundamentally: the service profits even if savings disappear within three months. The math favors you only if the negotiated rate holds and the fee remains proportional to actual, sustained benefit. Read the terms before connecting any account.

Does Truebill offer privacy controls that align with your risk tolerance?

Subscription apps and budgeting tools often describe broad account access as a convenience rather than a data risk. Linking a full bank account through a third-party aggregator lets the app see every transaction, not just the recurring ones it needs. Look for platforms that offer manual entry, granular permission settings, or read-only access modes. SOC 2 certification and clear third-party data-sharing disclosures are basic requirements, not extras.

How do default permissions in apps like Truebill compound your data exposure?

Most consumers accept default permissions because onboarding flows make full access feel required—it rarely is. As financial apps multiply and data broker ecosystems expand, those permissions compound into a profile extending well beyond subscription management. Sparrow takes a narrower approach, focusing on class action settlement discovery and claims filing rather than requiring broad financial access, keeping data exposure proportional to the task.

Cancellation Results You Can Verify

Top-rated alternatives have a 4.9/5 rating based on 10,500 reviews. The difference between high-rated tools and average ones comes down to functionality: did the cancellation go through, is there a confirmation to reference, and does the app follow up if the charge reappears? Tools that only send cancellation requests without confirmation leave users exposed to the billing inertia they sought to escape.

Why does Truebill-style confirmation matter for durable results?

Money you are legally owed or already saved should not require constant vigilance to protect. Whether that means a confirmed subscription cancellation, a locked-in negotiated rate, or a class action settlement payout you filed before the deadline, the standard is the same: the result should be durable, documented, and yours without ongoing effort.

The simplest tools often prove the most powerful, and that tension is where the next piece gets interesting.

Related Reading

- Nightfall Group Lawsuit

- Gmail Class Action Lawsuit

- Temu Lawsuit

- AT&T Class Action Lawsuit

- Amazon Prime FTC Settlement Lawsuit

- Minnesota Ice Lawsuit

- Life360 Lawsuit

- Turbotax Lawsuit

- Costco Sonoma County Lawsuit

- Amazon Fire Tv Stick Lawsuit

- Capital One Class Action Lawsuit

- Hexclad Lawsuit

- Apple Class Action Lawsuit

- Isotonix Lawsuit

- Dapper Development Lawsuit

10 Truebill Alternatives for Better Money Management

Truebill, now rebranded as Rocket Money, helps users make budgets, watch subscriptions, negotiate bills, and track spending. Some alternatives go even further by helping you recover unclaimed funds, find forgotten assets, make the most of your savings, or automate other parts of your financial life. The right choice depends on whether your priority is finding missing money, making a budget, improving your credit, or tracking your overall financial health.

“The best personal finance tool isn’t the most popular one — it’s the one actually built for your specific financial goals.”

💡 Tip: Before committing to any Truebill alternative, identify your #1 financial priority — whether that’s subscription tracking, credit improvement, or uncovering lost money — so you choose a tool that truly fits your needs.

⚠️ Warning: Many users default to the most well-known app without comparing features. The wrong tool can mean missing out on recovered funds, better savings rates, or smarter budget automation.

1. Sparrow

Sparrow finds and simplifies claims for class action settlements and related funds that users often miss, delivering an average of over $345 per year in possible recoveries without the percentage-based success fees or bank-linking requirements that reduce earnings in subscription and bill management tools.

Key Features

- Scans and delivers new no-proof class action settlements weekly, capturing opportunities that basic subscription trackers miss.

- Automatically prints and mails physical claim forms with postage included, eliminating manual paperwork.

- Money-back guarantee ensures users earn more than the subscription cost or receive a refund.

- Pre-fills claim forms with user information for quick submission.

- Matches users to high-value settlements such as Comcast Xfinity (up to $10,000) or Flo Period Tracker (up to $700).

- Tracks claim status and deadlines, such as 63 days remaining for the Disney/YouTube TV settlement.

- Focuses on no-proof-required claims, eliminating the need for receipts or documentation.

- Provides access to multiple active claims simultaneously (often 9+).

- Weekly emailed updates on new lawsuits arising from consumer protection violations, such as data breaches or false advertising.

Pros

Simplifies complex filing into minutes, offers a low annual cost with an earnings guarantee, uncovers passive settlement funds most consumers never pursue, and provides a convenient, mobile-friendly process.

Cons

Recoveries depend on settlement administrators and timelines, not on instant processing like some cancellations, and focus specifically on class actions rather than on daily budgeting or negotiations.

Accessibility

Web-based platform accessible via browser on phones and computers; annual plan at $7 per month ($84 billed yearly).

2. Monarch Money

Monarch Money provides a complete personal finance dashboard that excels at tracking and shared budgeting, offering deeper insights without charging negotiation fees.

Key Features

- Customizable budgeting with shared household access.

- Net worth and investment tracking that work together smoothly.

- Accurate sorting of transactions and identification of recurring expenses, with manual override options for privacy.

- Goal-setting and planning tools for long-term savings.

- Strong reporting and insights without success-based charges.

- Bank syncing with a strong focus on security.

- Collaborative features for couples or families.

Pros

Modern design, excellent for staying in control and seeing what’s happening, is often praised for accuracy.

Cons

Requires linking your bank account; annual fees can add up without robust cancellation support.

Accessibility

Web and mobile apps; subscription model around $99/year or similar monthly options.

3. YNAB (You Need A Budget)

YNAB focuses on active zero-based budgeting, teaching users to assign every dollar a purpose before spending it, which stops overspending.

Key Features

- Zero-based envelope system for intentional spending.

- Detailed educational resources and workshops.

- Real-time tracking with age-of-money metrics.

- Goal-oriented planning that reduces reliance on cancellations.

- Strong reporting on spending habits.

- Cross-device synchronization.

- Community support for behavior change.

Pros

Builds lasting financial habits; demonstrates high user success in debt reduction and savings.

Cons

Steeper learning curve; primarily budgeting, with no built-in negotiation.

Accessibility

Web, iOS, Android; $14.99/month or an annual discount available.

4. Quicken Simplifi

Quicken Simplifi offers clean bill tracking, projected cash flow, reliable automation, and clear forecasts, all without percentage-based fees.

Key Features

- Automated spending plan based on income and bills.

- Custom savings goals and watchlists.

- Accurate bill reminders and tracking.

- Simplified reports and visualizations.

- Household sharing options.

- Strong mobile experience.

- Integration for recurring expense management.

Pros

User-friendly for daily oversight; good value for bill-focused users.

Cons

Less emphasis on subscription auto-cancellation.

Accessibility

Web and mobile: affordable monthly or annual plans with frequent discounts.

5. PocketGuard

PocketGuard provides straightforward subscription tracking and bill negotiation tools at a competitive price, simplifying “in my pocket” spendable cash calculations while addressing fee concerns.

Key Features

- Subscription detection and cancellation assistance.

- Bill negotiation tools with potentially lower fees.

- “In My Pocket” feature for daily available funds.

- Basic budgeting and tracking.

- Expense categorization.

- Alerts for unusual charges.

- Mobile-first design.

Pros

Affordable, focused on simplicity for overwhelmed users.

Cons

May lack depth in advanced budgeting or investments.

Accessibility

Free tier available with premium upgrades on iOS and Android.

6. Copilot Money

Copilot Money offers AI-enhanced finance tracking with smarter insights and cleaner interfaces than Rocket Money, focusing on proactive spending analysis and subscription management. It surfaces patterns Rocket Money’s more basic dashboards might miss.

Key Features

- AI-powered categorization and predictive insights for better forecasting.

- Elegant subscription detection with visual trends.

- Net worth monitoring alongside daily expenses.

- Custom tags and advanced search for deep analysis.

- Privacy-focused syncing options.

- Beautiful reporting and visualizations.

- Goal tracking with progress alerts.

Pros

Modern, intuitive design; strong for users seeking intelligence over automation.

Cons

May require learning its AI suggestions; subscription pricing.

Accessibility

iOS- and Android-focused; monthly or annual plans.

7. EveryDollar

EveryDollar, backed by Dave Ramsey principles, offers simple zero-based budgeting to help users take back financial control. It contrasts with Rocket Money’s subscription-heavy approach by addressing spending leaks before they become significant problems.

Key Features

- Simple zero-based budgeting interface.

- Debt snowball integration for recovery focus.

- Manual or linked transaction entry.

- Baby Steps progress tracking.

- Basic subscription awareness through categories.

- Reports tied to financial peace principles.

- Free core version availability.

Pros

Free tier is robust; motivational framework for long-term savings.

Cons

Less automated than Rocket Money for cancellations.

Accessibility

Web and mobile apps with premium upgrades for added features.

8. Goodbudget

Goodbudget uses a shared-envelope system for collaborative budgeting, helping families recover from overspending by making fund allocation visible. This differs from Rocket Money’s individual-focused tracking.

Key Features

- Digital envelope allocation for every dollar.

- Real-time shared access for couples or families.

- Transaction assignment to envelopes.

- Historical reporting on envelope usage.

- Subscription categorization tools.

- Sync across devices.

- Educational budgeting guidance.

Pros

Excellent for transparency in shared finances; prevents hidden drains.

Cons

More manual effort required initially.

Accessibility

Web, iOS, Android; free with premium options for additional envelopes.

9. Empower (formerly Personal Capital)

Empower combines free net worth tracking with investment insights, helping you recover money through better wealth oversight than Rocket Money offers, especially for users with assets beyond checking accounts.

Key Features

- Comprehensive net worth dashboard.

- Investment portfolio analysis.

- Retirement planning tools.

- Cash flow and spending tracking.

- Free basic access with advisor options.

- Bill and subscription visibility.

- Secure bank and investment linking.

Pros

Robust for higher-net-worth users; no cost for core tools.

Cons

Less focused on everyday consumer subscriptions.

Accessibility

Web and mobile: free with premium services.

10. Trim

Trim acts as a direct bill negotiation and subscription specialist, offering more targeted recovery than Rocket Money and competitive fee structures to lower recurring costs.

Key Features

- Automated bill negotiation for services like cable and insurance.

- Subscription cancellation assistance.

- Savings tracking with clear reporting.

- Lower percentage fees in some cases.

- Expense reduction recommendations.

- Account monitoring alerts.

- User-friendly cancellation flows.

Pros

Strong focus on direct savings actions.

Cons

Still uses success fees; requires account access.

Accessibility

Web and app; fee-based on savings or subscription.

Tips for Choosing the Best Truebill Alternative

The best Truebill alternative solves your specific financial problem. Some platforms are great at budgeting, others focus on investments or debt reduction, while a few help you get money you didn’t know you were owed. Comparing your goals against what each platform delivers ensures you choose a tool that creates measurable financial value.

“The right financial tool isn’t the most popular one — it’s the one precisely matched to your specific money goals and spending habits.” — Personal Finance Best Practices

💡 Tip: Before committing to any platform, list your top 3 financial priorities — whether that’s cutting subscriptions, building savings, or tracking investments — and match them directly to what each tool offers.

🎯 Key Point: Not every alternative is built the same — matching your financial goals to the right platform is the single most important step in choosing a Truebill alternative that delivers real, measurable results.

Prioritize Transparent and Predictable Pricing

Look at the full cost structure, including hidden fees for premium features or negotiations. Rocket Money’s Premium ranges from $7 to $14 monthly, with additional 35-60% success fees on bill savings, which can offset benefits if reductions prove temporary. Credible reviews show how such models lead to disputes over claimed savings. Choose alternatives with flat annual fees or strong free tiers that clearly explain what is included.

Evaluate Subscription Detection Accuracy and Cancellation Ease

Test how well the app finds recurring charges and helps you cancel them with different merchants. Good tools sync reliably, catch duplicates, and let you cancel directly. Since the average American spends $219 monthly on subscriptions, often far more than they realize, this feature saves significant money without extra effort. It helps you overcome the inertia and design tricks that keep unwanted services running.

Assess Data Privacy and Security Standards

Look at how the platform handles data, how it protects information with encryption, and whether you must fully connect your bank account. Many users worry about data aggregators and information sharing, as evidenced by consumer complaints. Good alternatives let you enter information manually or offer better privacy controls, reducing exposure risk while providing the insights you need.

Check Budgeting Depth and Reporting Capabilities

Look for customizable budgets, spending categories, and helpful reports to support smart financial decisions. The best options offer net worth tracking, goal setting, and household sharing, helping users address broader cash flow issues rather than isolated cancellations.

Verify Bill Negotiation or Lowering Effectiveness

Look into how well bill reduction services work, what they charge, and what results customers get. Avoid services that promise exceptionally high savings percentages. Instead, choose ones that are transparent about their fees or charge limited fees and that can demonstrate proven results. Before signing up with any service, check independent reviews and reports to verify their performance.

Consider Customer Support and Ease of Use

Choose apps with good customer support, clear designs, and easy setup. Reliable tools reduce frustration during setup and troubleshooting, which matters when handling sensitive financial information. User ratings on major app stores and third-party sites reveal what real people think about the app.

Test for Long-Term Value and Exit Flexibility

Make sure the service offers trial periods, easy cancellation, and features that scale with your needs, such as investment tracking or advanced analytics. This prevents lock-in and lets you adapt as your financial situation changes.

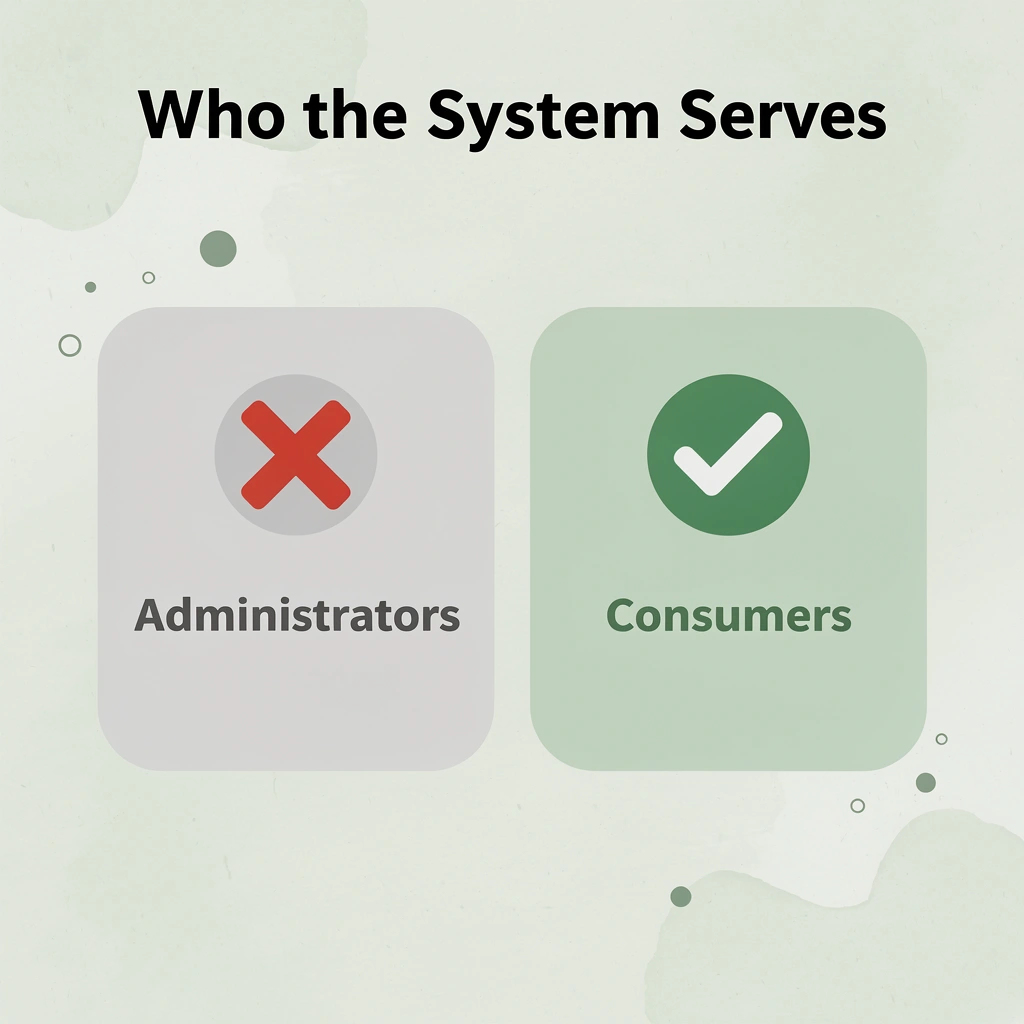

How Sparrow Makes Recovering Unclaimed Money Simple

Scattered databases, separate claim portals, and dozens of individual deadlines are not just an inconvenience — they are a design problem. The system was built for administrators, not consumers. Sparrow reverses that architecture, putting the consumer at the center instead of the paperwork.

“The system was built for administrators, not consumers — Sparrow reverses that architecture entirely.” — Core Design Philosophy

💡 Tip: Instead of navigating dozens of separate portals and deadlines on your own, let Sparrow consolidate the entire process into one seamless experience.

🎯 Key Point: Sparrow’s consumer-first design eliminates the friction of scattered databases and fragmented claim systems — so you stay in control, not the paperwork.

Why do so many people miss money they are owed?

The problem isn’t that people don’t want to find their money; it’s that money can be hidden in so many different places. According to Sparrow via GlobeNewswire, 1 in 10 Americans has unclaimed money waiting across state databases, expired gift cards, dormant accounts, and class action settlements. Knowing something is owed to you but facing so many search options leaves people unsure where to start, and most give up before trying.

How does Sparrow compare to tools like Truebill for filing claims?

Joining class action lawsuits through Sparrow breaks the cycle of sporadic searching and missed deadlines. Our platform scans for eligible settlements weekly, pre-fills claim forms with your details, and mails completed submissions with postage included. Seven claims filed in five minutes is what the process should have looked like from the start.

What makes this different from a simple reminder tool?

A reminder tells you that a deadline exists. Sparrow handles the step most people skip: the actual filing. Our forms get filled in ahead of time, printed, and mailed. Deadlines get tracked in a single dashboard alongside claim statuses. Settlements like the Disney/YouTube TV antitrust case (up to $200) or Toyota Airbags (up to $250) stay visible with exact days remaining, so nothing slips through a crowded inbox. That completion—not awareness—turns eligible consumers into paid claimants.

How does the guarantee compare to what Truebill offers subscribers?

At $84 per year, Sparrow backs the subscription with a money-back guarantee: recover more than you paid or get a refund of the difference. This removes the risk calculation entirely. The incentives are already aligned in your favor, and the only remaining question is how much you recover above the threshold.

Why does unclaimed money keep accumulating for most people?

Unclaimed money is a built-in part of how companies operate, not a mistake. Companies collect fees, settle lawsuits, and hold balances because most people won’t claim what they’re owed. Tools that simplify recovery shift the balance of power and reveal money people never knew they had.

Start Finding Money You May Be Owed with Sparrow

Budgeting tools manage what you have. They don’t recover what companies already owe you. Join class action lawsuits with Sparrow, which closes that gap by finding eligible settlements, making the filing process simpler, and tracking claims all the way to payout—removing the exact obstacles that stop most people from collecting money that is legally theirs.

“Most people never collect settlements they’re entitled to—not because they’re ineligible, but because the discovery and filing process is too complex to navigate alone.” — Sparrow

💡 Tip: There’s a critical difference between tools that manage your money and tools that recover it. Sparrow is built for the latter.

Visit Sparrow, create your account, and let our platform scan for settlements you qualify for. A few minutes of setup can uncover opportunities you’d never discover manually, all backed by Sparrow’s money-back guarantee on first-year payouts.

🎯 Key Point: Sparrow’s money-back guarantee means there’s no risk to getting started—your first-year payouts are protected.

✅ Best Practice: Don’t wait to sign up. Unclaimed settlements have deadlines, and each day you delay risks a qualifying payout slipping away.

Related Reading

- At&t Lawsuit

- Fortnite Lawsuit

- Celsius Lawsuit

- Poppi Lawsuit

Leave a Reply